The Federal Reserve should declare an immediate cease fire in its war against inflation and hold its benchmark interest rate steady instead of raising the federal funds by a half percentage point to a range of 4.25% to 4.50%, as expected at its meeting that ends Wednesday.

With the relatively benign report on the consumer price index in November released on Tuesday, the Fed has now has “compelling evidence” that it has achieved its immediate goal of seeing a significant slowing in inflation.

The CPI was better than expected in November, with headline inflation rising just 0.1% (1.2% annualized) and core inflation up 0.2% (2.4% annualized).

Read: Inflation is slowing, but the fight is far from over

The U.S. stock market

SPX,

DJIA,

COMP,

on Tuesday initially greeted the CPI report as confirmation that the Fed could begin to let up, but by midday the realization hit that the Fed is going to keep hiking rates.

Market Snapshot: Dow clings to gain in final hour of trade as Wall Street gauges cooler inflation report, next Fed rate decision

Better than the media says

The CPI report was actually better than it’s being portrayed by the media, which continue to focus irrationally on year-over-year changes in inflation rather than looking at what has happened since the Fed began raising interest rates nine months ago. For instance, what are we to make of. this incoherent headline in the New York Times: “U.S. Inflation Cools as Consumer Prices Rise 7.1 Percent”?

If we don’t want to miss the turning points, we have to shorten our horizon to something less than a year, but not so short that it’s all noise and no signal. Three months is about right.

In March 2022, when the Fed first raised rates, inflation was accelerating. From January to March, the CPI had risen at an 11.3% annual rate. That was an alarming inflation rate which called for action by the Fed.

But then the Fed raised interest rates at six straight meetings, going from near zero to near 4% and now inflation is decelerating. From September to November, inflation rose at a 3.7% annual rate.

That is significant progress in the most relevant measure of inflation.

Read: Why November’s CPI data are seen as a ‘game-changer’ for financial markets

The wrong perspective

The progress is much less apparent when the figures are reported on a year-over-year basis, as most media outlets do. From November 2021 to November 2022, inflation rose 7.1% — but that figure is meaningless to our understanding of what the Fed has accomplished because that time frame also includes five months of high inflation from before the Fed acted.

Because rate hikes take some time to have an impact on prices and on the economy, they didn’t really start to bite until July. In the five months since then, inflation has slowed to a 2.5% annualized rate, noticeable to anyone who’s looking. The unprecedented rise in interest rates is working to cool off price increases.

The progress is even greater when you take into account that almost all of the inflation we’ve suffered recently is coming from higher rents, which are now rising at a 10% annual rate in a lagged response to last year’s incredible 20%+ increase in home prices and tight rental markets.

Rents still rising as home prices fall

Home prices have now begun to fall in most regions of the U.S. Rents for new tenants have also begun to fall, but rents paid by continuing tenants have lagged behind and could take another year or longer to catch up, according to research by economists at Goldman Sachs. That’s because rents on existing leases tend to reset on an annual basis.

“ Rents are used to compute the costs not only of renters but of homeowners as well. It’s as if we measured champagne prices by looking at how much beer costs. ”

With more than 900,000 multifamily housing units now under construction, the supply constraints will soon begin to ease, reducing pressure on rents, when those units hit the market, likely in the next year or so.

Rents have an outsized influence on the CPI, because rents are used to compute the costs not only of renters but of homeowners as well. It’s as if we measured champagne prices by looking at how much beer costs. Yes, there’s some correlation most of the time, but not always.

Using rents to measure homeowners’ costs might be an acceptable methodology in normal times, but not now. Based on the increase in rents, the CPI showed that shelter costs for homeowners rose at a 8% annual rate in November. No one believes that’s true. Most homeowners have a fixed-rate mortgage, so principal and interest payments haven’t gone up.

The right perspective

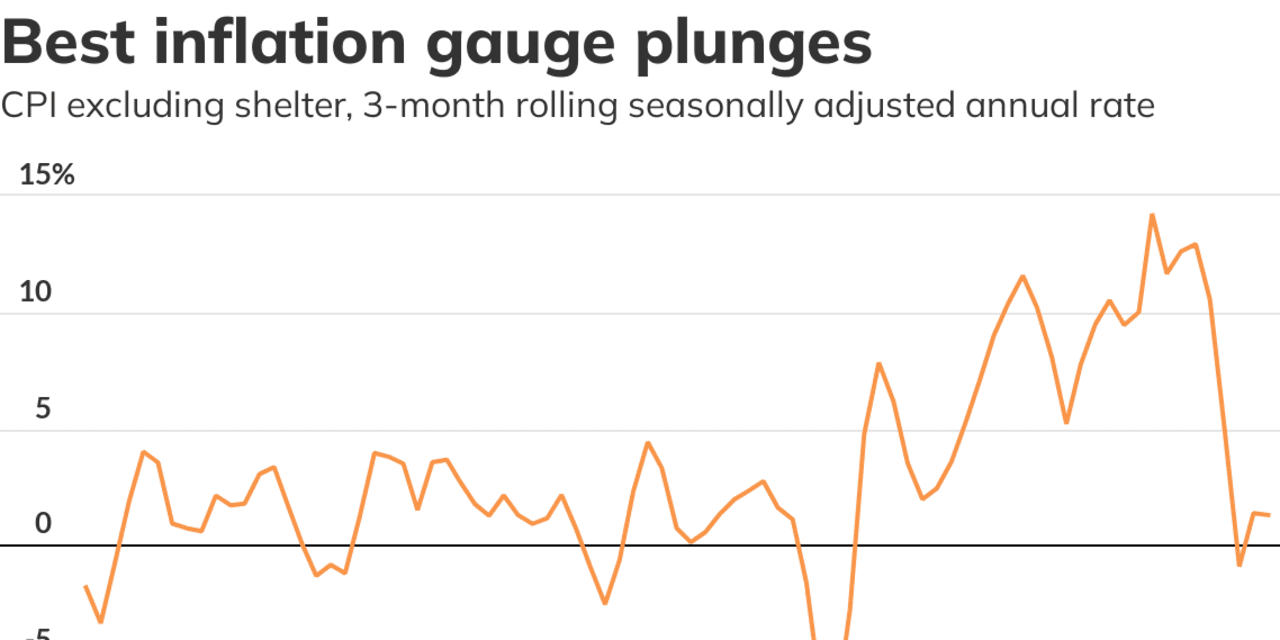

The best thing to do in this situation is to recognize that we need to exclude shelter costs (which accounts for a third of the CPI) if we want to see where underlying inflation is heading.

“Substantial disagreement about the correct way to measure shelter inflation argues for looking at inflation measures that put less weight on shelter inflation, not more, when the decision is of greater consequence,” wrote Goldman Sachs economists Ronnie Walker and David Mericle in a note published in October.

The CPI excluding shelter fell 0.2% in November and has risen at just a 1.3% annual rate over the past three months.

Even Fed Chair Jerome Powell has acknowledged that a sudden drop in home prices won’t show up in the headline CPI for months, but he’s not acting like he quite believes it. If he did, he’d urge his colleagues at the Fed to pause now and let the full impact of 375 basis points of tightening work on the economy.

More: Fed seen slowing down to quarter-point hike in February after soft consumer price inflation reading

We know, however, that the Fed won’t pause. The Fed lost too much credibility last year when it missed the rapid increase in inflation as the economy emerged from its pandemic lockdown, and now the Fed is scrambling to restore the public’s trust as an inflation fighter.

Unfortunately, that makes a recession nearly inevitable, because the Fed is going to do what it always does: Raise rates too far and push the economy into a job-killing recession.

Rex Nutting is a columnist for MarketWatch who has been writing about the Fed and the economy for more than 25 years.

Rex Nutting on inflation

What NASA knows about soft landings that the Federal Reserve doesn’t

Bigger paychecks are good news for America’s working families. Why does it freak out the Fed?

Share this news on your Fb,Twitter and Whatsapp

Times News Network:Latest News Headlines

Times News Network||Health||